Planning for Retirement as a Business Owner: Transforming Enterprise Value into a Lasting Legacy

The value of your life’s work is not found in the balance of a bank account, but in the enduring strength of the enterprise you have built. Many owners find their wealth is a silent partner, trapped within the illiquid equity of a business that still requires their constant presence to breathe. You likely feel the weight of this dependency, wondering if the precision you’ve applied to your craft has also been applied to your eventual exit. Planning for retirement as a business owner is often misunderstood as a simple exercise in tax-advantaged savings; in reality, it is a pursuit of transferability.

You’ll learn how to transform your company from a personal income source into a sophisticated, transferable asset that thrives independently of your daily oversight. As we look toward the December 31, 2026, deadline for SECURE 2.0 amendments, the landscape of stewardship is shifting. We provide a clear roadmap to financial independence by focusing on enterprise value growth and risk reduction. This article details the structural evolution required to ensure your business maintains its soul while providing the confidence that your legacy is both measurable and secure.

Key Takeaways

- Shift your perspective from viewing the business as a source of income to treating it as a transferable asset that functions as your primary retirement vehicle.

- Identify the "Value Gap" between your current enterprise valuation and your future financial needs to create a measurable target for strategic growth.

- Learn why planning for retirement as a business owner requires systematically reducing owner dependency to ensure the company remains valuable without your daily presence.

- Implement a structured three to five year roadmap that focuses on improving transferability and preparing the enterprise for a successful transition.

- Understand the importance of a "Quarterback" advisor who coordinates your professional team to ensure all strategic and financial elements of your legacy are aligned.

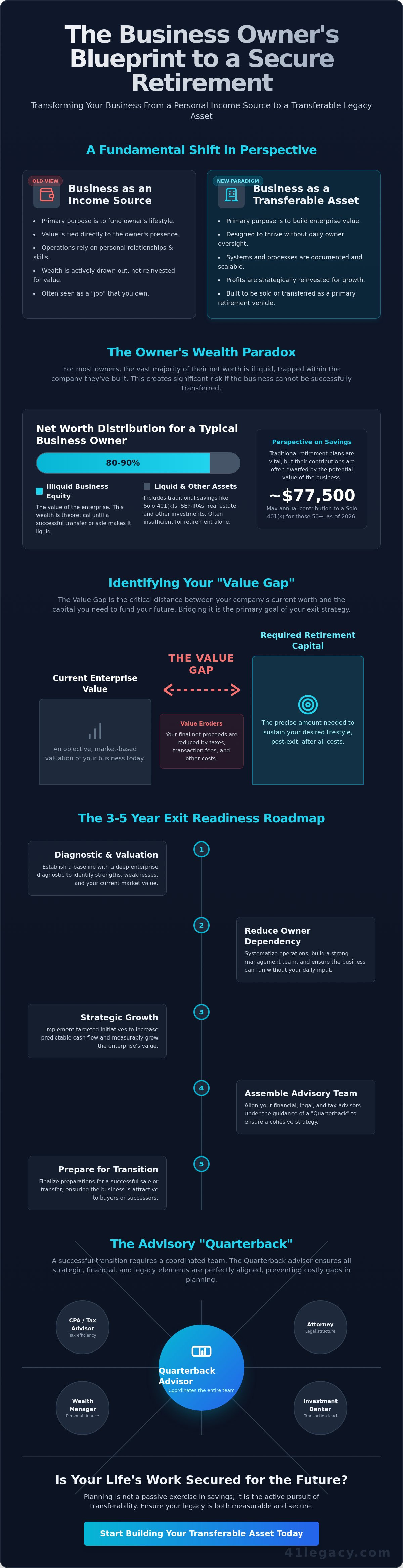

Redefining Retirement: The Business as Your Primary Asset

For most professionals, retirement is a countdown toward a specific date on a calendar. For the founder, this transition is less about time and more about a singular liquidity event. True planning for retirement as a business owner requires a fundamental shift from managing accounts to cultivating an asset. You aren't just saving for a future; you're engineering a machine that can eventually operate without you. This requires moving beyond the traditional comprehensive retirement planning models that prioritize passive savings over active asset optimization.

The Reality of Business-Centric Net Worth

Traditional tools like the SEP-IRA or Solo 401(k) serve a vital purpose, but they are often secondary to the enterprise itself. In 2026, the contribution limit for a Solo 401(k) is $70,000, which increases to $77,500 for those age 50 or older. While these figures are useful for tax diversification, they rarely capture the full scope of an owner's wealth. Statistics suggest that for the majority of private business owners, 80% to 90% of their net worth is "trapped" within the equity of their company. This illiquidity creates a significant risk. If the business cannot be transferred or sold, that wealth remains theoretical. To mitigate this, you must adopt the perspective of a steward, ensuring the company is attractive to an external buyer or an internal successor.

Enterprise Value vs. Lifestyle Income

There is a critical distinction between a company that funds a lifestyle and one that possesses enterprise value. Many owners build successful lifestyle businesses that provide excellent annual income but lack the internal structure to survive a transition. If the business relies on your personal relationships or technical mastery to function, it's a job, not a transferable asset. Building a legacy requires a meticulous focus on reducing owner dependency. The goal is to move from a business that merely pays the bills to one that has a measurable, market-ready value. At 41 Legacy, we view this transition as a form of high-end restoration. The engine of the business must be tuned to run autonomously, ensuring your life's work retains its soul and its value for generations to come.

Identifying the Value Gap in Your Retirement Strategy

Precision in engineering requires a baseline. Without a clear starting point, you cannot measure progress or ensure the integrity of the final result. In the context of planning for retirement as a business owner, this baseline is your current enterprise value. The "Value Gap" represents the mathematical distance between the net proceeds you will receive upon a future exit and the capital required to sustain your desired lifestyle. Many owners operate under the optimistic assumption that their business will naturally bridge this gap. However, market data consistently reveals a significant disconnect between owner expectations and the cold reality of a professional valuation.

A successful transition depends on an objective analysis of the facts. While you may have spent decades perfecting your craft, the market values a company based on its predictable future cash flow and its ability to function without your direct intervention. Overestimating worth is a frequent pitfall. It's often driven by the emotional weight of years of dedication rather than the clinical metrics a sophisticated successor uses to judge an asset. Bridging this gap is the primary objective of a strategic growth plan.

Calculating Your Retirement Needs

Defining your "number" involves more than just a lifestyle estimate. You must account for the inevitable erosion of value through taxes and transaction costs. For instance, a headline sale price of several million dollars may result in significantly less liquidity after state and federal obligations are settled. When exploring various retirement plan options for business owners, it's vital to integrate these traditional savings vehicles with the projected liquidity from your business asset. This holistic view ensures you aren't leaving your financial future to chance. You must determine the exact amount of capital required to fund your post-exit life, then work backward to see if your current enterprise value meets that threshold.

The Role of Enterprise Diagnostics

Strategic clarity begins with a diagnostic. This is not a simple opinion of value, which often lacks the depth required for true asset optimization. A diagnostic identifies the structural risks that suppress your valuation multiple. It reveals where the internal machinery of your company is leaking value. By establishing this baseline, you can begin planning for retirement as a business owner with a strategy that focuses on high-impact improvements. Identifying these friction points early allows you to build a strategic roadmap that elevates the enterprise from a personal income source to a high-performance asset. This diagnostic phase is the cornerstone of a predictable transition, providing the confidence that your life's work has reached its full potential.

The Transferability Trap: Reducing Owner Dependency

Many founders believe their personal touch is the company’s greatest asset. In reality, for anyone planning for retirement as a business owner, this dependency is often the greatest liability. A business that cannot function without its founder isn't an asset; it's a high-stakes job. We call this the transferability trap. It occurs when the "Master Craftsman" realizes their personal excellence prevents the enterprise from reaching a state of permanence. To build a lasting legacy, you must engineer the business to thrive in your absence. This shift requires a meticulous transition from a creator of value to a steward of systems.

The emotional weight of stepping back shouldn't be underestimated. It’s a philosophical evolution to acknowledge that the company's soul must eventually exist outside of your own. When you reduce your daily presence, you aren't diminishing your importance. You're actually elevating the business to its highest form. This process of "Transferability Engineering" ensures the engine of your life's work continues to hum with precision long after you have moved on to your next chapter.

The Rainmaker Trap

The "Rainmaker Trap" is a specific vulnerability where the owner remains the primary architect of revenue or the lead technician. If you close every major deal or solve every technical crisis, the business’s value is tethered to your physical presence. Successors seek a machine that runs, not a visionary who must be present to keep the lights on. They view owner-centric operations as a high-risk investment. This risk often results in lower valuation multiples or structured earn-outs that keep you tied to the desk long after you intended to exit. Delegating authority is a financial necessity, not just a management preference.

Building Systems and SOPs for Exit Readiness

Documented processes act as the blueprints for a transferable legacy. Standard Operating Procedures (SOPs) transform individual talent into institutional knowledge, creating a "turnkey" asset that a new steward can operate with confidence. While you navigate the complexities of IRS retirement plan regulations to secure your personal capital, these internal systems secure your enterprise value. Meticulous documentation signals to the market that the company’s success is repeatable and scalable. Building a transferable legacy requires this uncompromising focus on process maturity. It ensures the soul of the company remains intact even as the hands at the wheel change.

The Exit Readiness Roadmap: A Structured Approach

A legacy is not built in a single season. It requires a deliberate, multi-year progression from active management to passive stewardship. Successful planning for retirement as a business owner typically demands a three to five year horizon to ensure the enterprise is fully de-risked and optimized for transition. This window allows you to move beyond the immediate pressures of daily operations and focus on the structural integrity of the asset. By viewing the company as a future legacy rather than a personal income stream, you become a steward of its long-term health. Implementation support during this phase ensures that strategic intent translates into operational reality.

Phase 1: Diagnostic and Valuation

The first stage involves determining the current altitude of the business through a rigorous analysis of internal and external factors. We identify the specific value drivers, such as financial hygiene and market positioning, that move the needle most for potential successors. An Exit Readiness Assessment serves as the essential foundation of any retirement plan, providing the objective data needed to make informed decisions. This phase strips away assumptions, revealing the hidden risks and untapped opportunities within the existing machinery of the company, which is a critical step in planning for retirement as a business owner.

Phase 2: The Value Growth Roadmap

Once the baseline is established, the focus shifts to prioritizing improvements that maximize transferability and increase profit. This isn't about incremental change; it's about a meticulous overhaul of the systems that define the company’s worth. A Value Growth Roadmap aligns daily operations with long-term exit goals, ensuring every action taken today contributes to the ultimate liquidity event. By setting measurable milestones, you create a clear path toward a business that can thrive independently. This structured approach provides the strategic clarity necessary to transform a private enterprise into a lasting, transferable legacy. To begin this transformation, you can connect with our advisory team for a preliminary consultation.

The Advisory Quarterback: Coordinating Your Retirement Team

A high-performance engine requires every component to fire in perfect synchronization. When planning for retirement as a business owner, your advisory team must operate with the same level of harmony. Most owners find that their CPAs, attorneys, and wealth managers work in silos, each focusing on their specific discipline without a shared vision for the enterprise. A CPA might focus on minimizing this year's tax liability; an attorney might focus on immediate risk mitigation. Without a central leader to coordinate these efforts, the strategic growth of the business can become fragmented, stalling the very value you intend to harvest.

The "Quarterback" role is essential for a successful transition. This central advisor, often a Certified Exit Planning Advisor (CEPA), ensures that every professional on your team is moving toward the same objective. They bridge the gap between your personal financial needs and the operational health of the company. By maintaining a professional-room altitude, this coordinator prevents technical specialists from making decisions that inadvertently damage the long-term transferability of the asset. This level of oversight ensures that your legacy is protected from the friction of misaligned advice.

Aligning Tax, Legal, and Strategic Decisions

Conflict often arises between short-term tax efficiency and long-term exit value. A tax strategy that maximizes immediate deductions might lower your reported earnings, which can unintentionally reduce the valuation multiple a successor is willing to pay. Similarly, legal structures must be reviewed through the lens of a future transfer, ensuring that contracts and governance documents don't create unnecessary hurdles during a transition. Your advisory team must protect the soul of the business while preparing it for a change in stewardship. This requires a meticulous review of how every legal and financial decision impacts the eventual liquidity event.

The Stewardship Mindset

The journey of planning for retirement as a business owner is a psychological evolution. You must transition from an Operator, deeply involved in the daily intricacies, to an Owner who focuses on strategy, and finally to an Investor who oversees the capital your life's work has generated. This shift requires the courage to trust the systems you have built. Preparing for the emotional weight of this transition is just as important as the financial engineering. At 41 Legacy, we believe that a well-executed exit is the ultimate expression of craftsmanship. It is the final act of a steward who has built something capable of outlasting their own tenure. If you are ready to begin the process of securing your legacy, we invite you to explore our advisory support to ensure your enterprise is prepared for its next chapter.

Securing the Future of Your Enterprise

Your business is more than a series of transactions; it's a testament to your vision and dedication. Transforming that vision into a liquid asset requires moving beyond the traditional boundaries of savings accounts to focus on the structural health of the company itself. By identifying your value gap and systematically reducing owner dependency, you ensure the enterprise retains its soul while gaining the independence to thrive under new stewardship. This evolution allows you to step away with the confidence that your life's work is both measurable and secure.

Planning for retirement as a business owner is a deliberate process that demands professional-room precision. Our strategy, led by a Certified Exit Planning Advisor (CEPA), utilizes a structured Value Growth Roadmap to align your daily operations with your ultimate legacy goals. We act as the advisory quarterback, coordinating your legal and financial experts to ensure every decision strengthens the transferability of your asset. You've spent a career building something extraordinary; now is the time to ensure its permanence and your financial freedom.

Begin your journey toward a transferable legacy with an Exit Readiness Assessment. Your dedication deserves a transition that is as meticulous and uncompromising as the business you created.

Frequently Asked Questions

Is my business my retirement plan?

Your business is likely your primary retirement asset, representing 80% to 90% of your total net worth. However, it only functions as a retirement plan if it's transferable. Without a clear strategy to convert enterprise value into liquid capital, that wealth remains theoretical. You must shift from an operator mindset to a stewardship mindset to ensure the company can eventually fund your post-exit lifestyle.

What is the difference between exit planning and retirement planning?

Retirement planning focuses on personal financial needs and tax-advantaged accounts like IRAs. Exit planning is a business strategy that focuses on maximizing enterprise value and ensuring the company can thrive without you. While retirement planning asks how much you need, exit planning asks how to build an asset that the market wants to buy. Both must be coordinated for a successful transition.

How many years before retirement should I start exit planning?

You should begin the exit planning process three to five years before your anticipated transition date. This timeline is necessary to implement a Value Growth Roadmap and address structural risks like owner dependency. Rushing the process often results in lower valuation multiples or unfavorable deal terms. Starting early allows you to fine-tune the business engine, ensuring it operates with the precision required for a high-value liquidity event.

Why do I need an Exit Readiness Assessment if I'm not selling yet?

An Exit Readiness Assessment provides a baseline for your company's current altitude and identifies hidden risks that suppress value. Even if a sale is years away, knowing your Value Gap allows you to prioritize improvements that increase transferability. It transforms vague assumptions into a measurable strategy. This diagnostic ensures that when you're ready to sell, the enterprise is already optimized for a premium offer.

Can a business be sold if it relies entirely on the owner?

A business that relies entirely on the owner is difficult to sell and often commands a significantly lower valuation. Sophisticated successors seek a turnkey asset, not a job where they must replicate your specific technical mastery or personal relationships. If the soul of the company is tethered to your daily presence, the risk to a buyer is too high. Reducing this dependency is the core of planning for retirement as a business owner.

What is the role of a Certified Exit Planning Advisor (CEPA)?

A Certified Exit Planning Advisor (CEPA) acts as the strategic quarterback for your retirement team. They coordinate the efforts of your CPA, attorney, and wealth manager to ensure every decision aligns with your legacy goals. By focusing on value acceleration, a CEPA helps you build a more valuable and transferable company while simultaneously preparing your personal finances and life for the transition.

How does owner dependency affect the valuation of my company?

High owner dependency acts as a drag on your valuation multiple, as it represents a significant operational risk for any successor. Buyers typically apply a discount to companies where the founder is the primary salesperson or lead technician. By documenting systems and delegating authority, you increase the company's transferability. This shift from a person-centric to a process-centric model is what ultimately drives a higher market price.

Do I still need a 401(k) or SEP IRA if I plan to sell my business?

You should maintain traditional retirement plans to provide tax diversification and a financial safety net outside of the company. In 2026, the contribution limit for a SEP-IRA is 25% of compensation, up to a maximum of $70,000. These accounts complement the liquidity event of a business sale. planning for retirement as a business owner requires a holistic approach where the business asset and personal savings work in tandem to secure your future.

Article by

Mike Laskowski

Mike Laskowski is a Business Value Growth Strategist who helps business owners uncover the truths that drive their performance, risk, and readiness. Blending forensic interviewing from a 26‑year federal career with Strategic Capacity analysis and CEPA methodology, he works upstream to reduce owner dependency, increase transferability, and strengthen enterprise value. Mike guides founders through clarity, operational evolution, and transition readiness so their companies become transferable, owner‑independent assets that endure beyond the founder.

Disclaimer

This article is for educational and informational purposes only and does not provide legal, tax, investment, or business brokerage advice. 41 Legacy does not offer M&A brokerage services, legal document drafting, tax preparation, or investment advisory services. Business owners should consult licensed professionals in those disciplines before making decisions related to business transactions, legal matters, tax strategy, or financial planning. All examples are illustrative and may not apply to your specific situation.